Subscribe to the NTA’s Blog and receive updates on the latest blog posts from National Taxpayer Advocate Nina E. Olson. Additional blogs from the National Taxpayer Advocate can be found at www.taxpayeradvocate.irs.gov/blog.

Over the years I have repeatedly raised concerns regarding the IRS’s Identity Theft (IDT) and non-IDT refund fraud programs. Most recently I expressed these concerns in testimony before the House Ways & Means Oversight Committee, my 2018 Annual Report to Congress and in two blog posts on December 6, 2018 and December 12, 2018. During the 2018 filing season, the IRS refund fraud programs were plagued with high false positive rates (above 80 percent in some cases) and long processing times, delaying legitimate refunds for about 40 days, which increase taxpayer burden, generate phone calls to the IRS, and result in Taxpayer Advocate Service (TAS) cases. High false positive rates and delays in taxpayers receiving their refunds were caused in part by the Internal Revenue Service’s (IRS) reliance on manual processes and failure to consider if holding the refund was appropriate. Specifically, I identified the following issues:

- A high number of legitimate returns being selected into the non-IDT refund fraud program: Between January 1 and October 3, 2018, the false positive rate (FPR) for non-IDT refund fraud filters was 81 percent, while the FPR for IDT refund fraud filters was 63 percent.

- Delays in receiving wage information: For filing season (FS) 2018, the IRS received 42 percent of expected employer/employee documentation on or by February 5, 2018, representing 43 percent of employee information documents.

- Technical problems with an IRS system requiring information and processes to be input manually: During FS 2018, because of system failures, returns were matched against W-2 information manually rather than systemically. Subsequently, the W-2 information needed to be manually entered and then refunds were manually released.

To improve the effectiveness of its non-IDT refund fraud program for FS 2019, the IRS has made several changes, including the following:

- It is systemically checking for the posting of third-party information daily instead of weekly.

- When the return is being selected due to a mismatch between the information on the return and the third-party information, the IRS will conduct additional analysis. If the third-party information would have no impact on the amount of the refund, the refund will be released immediately.

- When a return carries with it both an IDT and non-IDT refund fraud concern, IRS systems will have the capability to systemically verify income and withholding information while simultaneously working to authenticate the taxpayer’s identity, thereby compressing the processing time.

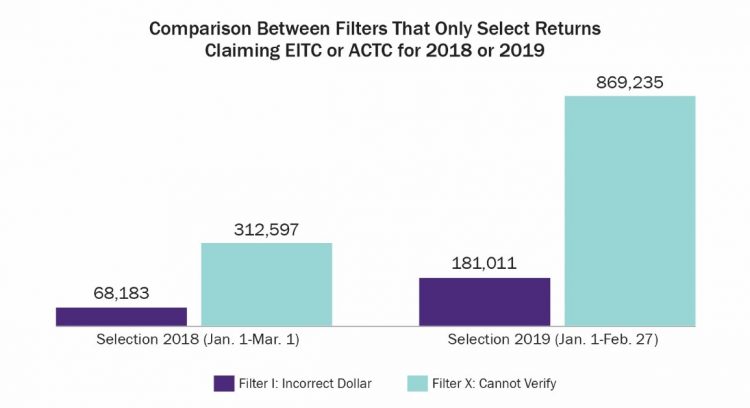

Although it is too early to draw any conclusions about the effect these changes have had on the refund fraud program, the data available thus far shows some noteworthy differences between the non-IDT refund fraud program for this filing season compared with last filing season. As shown in the figure below, according to a weekly deck provided to us by the IRS, the two non-IDT refund fraud filters that exclusively select returns where Earned Income Tax Credit (EITC) or Additional Child Tax Credit (ACTC) have been claimed more than doubled their selection of returns compared to last year.

Figure 1. Comparison Between Filters That Only Select Returns Claiming EITC or ACTC for 2018 or 2019

One possible explanation for this increase is the adoption of new systemic verification and reprocessing features for Filter X, which allows the IRS to increase its workload projections. According to customized data provided to us by the IRS, through February 27, while Filter X has selected about 869,235 returns, more than half of those returns have already been identified for release as shown in the figure below. Comparing these results with the same filter selections and release rates for the same period during 2018, Figure 2 indicates the IRS is doing a much better job at systemically identifying more returns for release earlier in the process.

Figure 2. Data Comparing Filter X Selections and Returns Identified for Release in 2019 to Selections Identified for Release for the Same Time Period During 2018

This noteworthy increase in refunds being identified for release is largely attributed to the IRS having over a hundred million more W-2s available at the beginning of February than it did last year, as shown in the figure below. The IRS received 219 million W-2s through February 4 this filing season, compared with 101 million for the same period last filing season – an increase of about 117 percent.

Figure 3. Information Return Master File (IRMF) W2 Data Availability Through February 4

The early submissions of W-2s allowed the non-IDT refund fraud program to perform pre-work on selected returns so the IRS could begin issuing EITC and ACTC refunds after February 15. Another contributing factor to the increase in returns being released is that the IRS now checks for the posting of W-2s daily instead of weekly.

If this early-release trend continues, I would expect that the non-IDT refund fraud program’s Operational Performance Rate (OPR), which is defined by the IRS as returns that are selected and not released by the pre-refund wage verification program within two weeks of selection, would decline. In a blog post from December 12, 2018 and in the 2018 Annual Report to Congress, I discussed in more detail the IRS’s calculation of the FPR and OPR, and I also recommended that the IRS track another data point that I have coined the “Operational FPR.”

However, the true test of the effectiveness of these changes will be the number of non-IDT refund fraud TAS case receipts for FS 2019. Overall, TAS received 11,431 non-IDT refund fraud cases during FS 2018 (from January 1 through March 9, 2018) compared to 20,610 cases for the same time period in 2019 – an increase of about 80 percent. However, the 2019 filing season case receipt numbers include tax year 2017 returns that are still coming into TAS inventory. Without counting cases involving prior years returns from the overall TAS case receipts, during FS 2019 (between January 1 and March 6, 2019) TAS received 4,634 non-IDT refund fraud cases compared with 6,062 cases received during the same period in FS 2018 (between January 1 and March 6, 2018), which constitutes about a 24 percent decrease.

Initial data indicates changes made to the non-IDT refund fraud program have resulted in a more effective fraud detection system that creates less burden for taxpayers. However, as the filing season rolls on and more data become available, TAS will continue to evaluate the impact of these changes.

The views expressed in this blog are solely those of the National Taxpayer Advocate. The National Taxpayer Advocate is appointed by the Secretary of the Treasury and reports to the Commissioner of Internal Revenue. However, the National Taxpayer Advocate presents an independent taxpayer perspective that does not necessarily reflect the position of the IRS, the Treasury Department, or the Office of Management and Budget.

Source: taxpayeradvocate.irs.gov

Leave a Reply