Subscribe to the NTA’s Blog and receive updates on the latest blog posts from National Taxpayer Advocate Nina E. Olson. Additional blogs from the National Taxpayer Advocate can be found at www.taxpayeradvocate.irs.gov/blog

In February of 2019, I released the 2018 Annual Report To Congress in which, among other things, I discuss the influence of tax audits on taxpayers’ attitudes and perceptions, and specifically focus on the three primary types of traditional or “real” IRS audits, which can occur through correspondence, at the taxpayer’s home or business, or at an IRS office. In my 2017 Annual Report to Congress and a related blog post around nine months ago, I described IRS audit rates and the distinction between “real” and “unreal” audits. This blog, however, provides an overview of traditional or “real” audit programs, along with some of my findings.

Why are IRS audits important?

The IRS is authorized to examine books, papers, records, or other data and take testimony to determine the correctness of any return and the liability of any person for tax under Internal Revenue Code (IRC) § 7602(a). The IRS’s primary purpose in selecting tax returns for examination or audit is to promote the highest degree of voluntary compliance. IRS audits are intended to detect and correct noncompliance of audited taxpayers, as well as create an environment to encourage non-audited taxpayers to comply voluntarily.

What Types of Audits are Conducted by the IRS Operating Divisions?

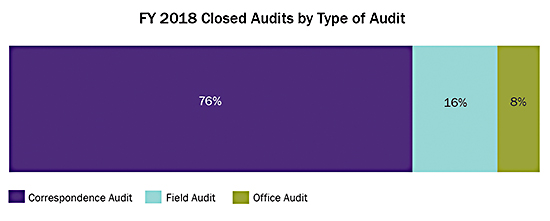

As stated above, the IRS conducts audits either via correspondence, office, or field audits. Generally, correspondence audits are managed by mail for a single tax year and involve no more than a few issues that the IRS believes can be resolved by reviewing simple documents. A field exam deals with more complex issues and involves a face-to-face meeting between the taxpayer and an IRS revenue agent at the taxpayer’s home or place of business. Finally, an office audit is conducted at a local IRS office and generally involves issues that are more complex than those found in correspondence exams, but less complex than examinations conducted in the field.

In fiscal year (FY) 2018, the IRS audited almost 970,000 taxpayer’s tax returns (including business and individual returns), approximately 0.5 percent of all returns received that year. Correspondence audits are by far the most common type of audit comprising approximately 76 percent of all audits (business and individual) as shown on the figure below.

In my report, I discuss examination programs operated by three IRS business operating divisions – Wage & Investment (W&I), Small Business and Self-Employed (SB/SE), and Large Business & International (LB&I).

- W&I handles taxpayers who pay taxes through withholding. W&I conducts all its audits via correspondence concerning issues such as refundable credits and some returns containing Schedule C, Profit and Loss from Business.

- SB/SE conducts correspondence audits, office audits, and field examinations of small business taxpayers with assets less than $10 million, as well as examinations of self-employed and other individuals with income that extends beyond the level of W&I responsibility.

- LB&I is responsible for the tax compliance of businesses with assets of $10 million or more, as well as individuals with high wealth or international tax implications. LB&I conducts field, office, and correspondence audits.

An overview of the audit selection process for each business operating division can be found in the Exam Introduction section, of my 2018 Annual Report.

What Do the Audit Results Show?

A TAS review of 2018 audit results by audit type reflected some of the strengths and weaknesses of the IRS’s examination programs in terms of promoting voluntary compliance.

- IRS office and field audits show high “agreed” rates of about 47 percent on average for each type of audit, but many of the field audits also concluded with “no change” in tax, suggesting that both SB/SE and LB&I are not identifying the correct tax returns or issues for audit.

- Combined W&I and SBSE correspondence audit results show a “non-response” rate of 40 percent and a default rate of 20 percent. The 40 percent “non-response” rate indicates that taxpayers did not respond at all to either the IRS’s correspondence audit notice or their resulting statutory notice of deficiency. In addition, another 20 percent of the taxpayers that did respond and participate in these examinations did not sign an agreement or petition the Tax Court after the issuance of the statutory notice of deficiency.

Of particular concern, is that most of these correspondence audits involved audits of individual income tax returns of low-income taxpayers with incomes of $25,000 or less who claimed the Earned Income Tax Credit (EITC). The high “non-response” and default rates among these taxpayers suggest that it is especially difficult for taxpayers who claim the EITC to respond to the IRS timely and appropriately for several reasons, including the complexity of EITC eligibility requirements and complicated family living situations.

In effort to determine the effectiveness of the IRS’s audit program, it is essential that we look at the factors that influence voluntary compliance. In next week’s blog, we’ll explore recent research into these factors, especially in the context of audits, and discuss the impact of IRS audits on voluntary compliance.

The views expressed in this blog are solely those of the National Taxpayer Advocate. The National Taxpayer Advocate is appointed by the Secretary of the Treasury and reports to the Commissioner of Internal Revenue. However, the National Taxpayer Advocate presents an independent taxpayer perspective that does not necessarily reflect the position of the IRS, the Treasury Department, or the Office of Management and Budget.

Source: taxpayeradvocate.irs.gov

Leave a Reply